Most people don’t know the difference between short-term and long-term disability insurance coverage until they have to. However, these differences can significantly impact your way of life if you need to file a claim for benefits.

Read on to learn more about short-term vs. long-term disability insurance and how these different types of plans work.

What we’ll cover:

- What is disability insurance?

- Short-term vs. long-term disability

- What does short-term disability insurance cover?

- What does long-term disability insurance cover?

- Insurance companies are not on your side

What is disability insurance?

Disability insurance is a type of insurance that provides financial support if you cannot work due to an illness or injury. It helps to replace some or all of the wages you would have earned if you could continue working, enabling you to maintain your lifestyle and pay your bills.

Many employers offer disability insurance as part of their benefits package, but it is also available through some insurance companies as an individual policy.

Read more: ERISA vs. Individual Disability Insurance

It’s more common than you might think for someone to become disabled and unable to work sometime during their lifetime. Statistics show that one in four 20-year-olds can expect to be out of work for at least a year before they retire because of a disability. Workers’ Compensation and Social Security Disability Insurance (SSDI) may not be enough to cover lost income during this time.

It’s more common than you might think for someone to become disabled and unable to work sometime during their lifetime.

The type of disability plan you have will determine the amount you’ll receive in disability benefits, when you receive them, and how long those benefits will last. It will also affect your chances of having your disability claim approved.

It’s important to understand the details of your plan to ensure that you are fully informed and know what to expect should you need to make a claim.

Some quick definitions

Before we dig into the specific differences between short-term and long-term disability, here are a few terms you should know.

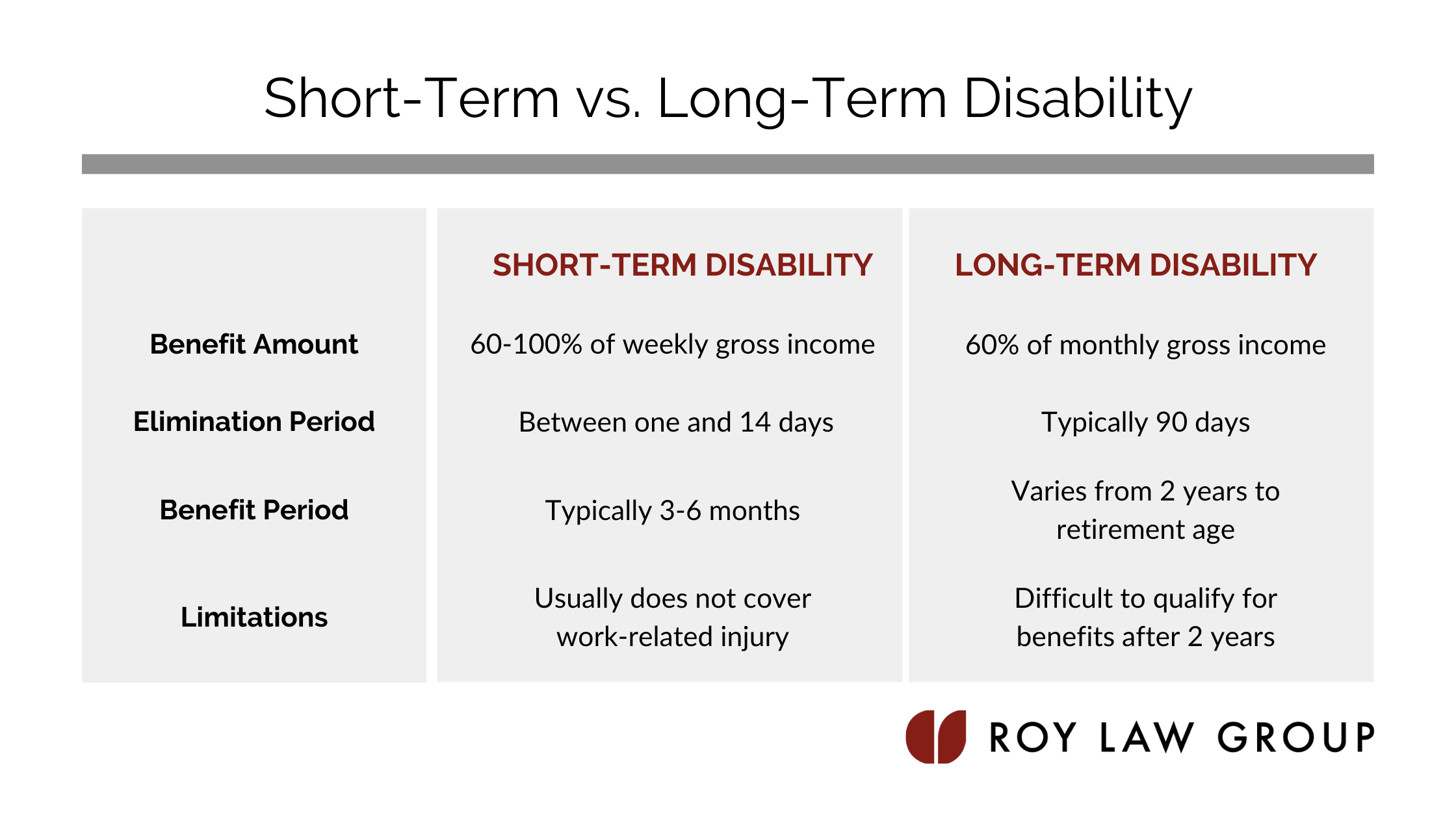

Benefit amount

A benefit amount in disability insurance is the amount of money you will receive if you become disabled due to a qualifying illness or injury and cannot work. This amount is typically a percentage of your pre-disability income and is intended to replace a portion of your lost income.

Elimination period

An elimination period, or waiting period, is the period of time between when you become disabled and when you will be eligible to start receiving benefits from your insurance company.

Benefit period

A benefit period is the length of time in which you may receive benefits for a qualifying claim.

Short-term disability vs. long-term disability

The main difference between short-term disability (STD) and long-term disability (LTD) insurance is the length of time for which they provide benefits. STD insurance provides benefits for a few weeks up to six months, while LTD insurance has you covered for a much longer period, often until retirement age, if necessary.

Another key difference is the elimination period, or waiting period, before benefits kick in. STD insurance usually has a shorter elimination period, often just a day or a few weeks, while LTD insurance usually has a longer waiting period, typically several months. This is because LTD insurance is designed to cover more serious, long-term disabilities, while STD insurance is meant to cover shorter-term, temporary disabilities.

Short-term disability and long-term disability can be used together or separately, depending on the circumstances. It is not an either/or choice. Long-term disability plans will often pick up where your short-term disability left off, allowing for a seamless transition from one benefit to the other.

Both of these types of disability benefits can provide financial stability in the event of an unexpected medical event, allowing you to focus on your recovery without having to worry about the financial implications.

What does short-term disability insurance cover?

Short-term disability (STD) insurance covers a percentage of your wages if you temporarily cannot work due to illness, injury, or pregnancy.

STD benefit amount

Short-term disability benefits typically cover approximately 60-100% of your weekly gross income. This is paid out as a lump sum or in installments.

STD elimination period

You can generally begin to receive short-term disability benefits between one and 14 days after you become disabled.

STD benefit period

Short-term disability benefits may last between three to six months, at which point long-term disability benefits may apply if you qualify.

STD limitations

Short-term disability is usually available through your employer’s benefit plan. However, you can also purchase coverage on your own. If you purchased your coverage, it is considered a stand-alone insurance policy. These individual plans can be pretty expensive and may not cover work-related injuries.

These policies generally define “disability” liberally and cover a wide range of situations with few restrictions or limitations on coverage.

Common reasons for short-term disability claims:

- Pregnancies (25%)

- Musculoskeletal disorders affecting the back and spine, knees, hips, shoulders, and other parts of the body (20%)

- Digestive disorders, such as hernias and gastritis (7.8%)

- Mental health issues, including depression and anxiety (7.7%)

- Injuries such as fractures, sprains, and strains of muscles and ligaments (7.5%)

Read also: 7 Reasons Short-Term Disability Can Be Denied

What does long-term disability insurance cover?

Long-term disability (LTD) insurance covers a percentage of your wages when you become injured or seriously ill for an extended period.

LTD benefit amount

Most long-term disability policies cover around 60% of your monthly gross income before becoming disabled. This does not include overtime, bonuses, or commission compensation. Your insurance policy documents define the length of coverage for your long-term policy.

LTD elimination period

Typically, your long-term policy will kick in once your short-term benefits have been exhausted. This is usually after around 90 days or three months.

LTD benefit period

LTD policies provide compensation anywhere from two years through age 65 or your Social Security retirement age, whichever is greater. This is only if you remain disabled under the policy, and your insurance company can decide to deny your benefits at any time.

Read more: Why Long-Term Disability Claims Get Denied

LTD limitations

LTD policies generally define disability more conservatively and contain many restrictions and limitations on the medical conditions they will cover. Often, long-term disability policies will become much more difficult to qualify for after 24 months of coverage.

Common reasons for long-term disability claims:

- Musculoskeletal disorders (29%)

- Cancer (15%)

- Pregnancy (9.4%)

- Mental health issues, including depression and anxiety (9.1%)

- Injuries such as fractures, sprains, and strains of muscles and ligaments (9%)

Read more: Medical Conditions That Qualify For Long-Term Disability

Insurance companies are not on your side

It’s important to keep in mind that insurance companies will go out of their way to find any reason to deny your disability claim. This applies no matter what kind of claim, but it is especially true for long-term disability claims. The insurance company’s interests are not aligned with yours, and they will instead focus on their profits.

Because your insurance company is not on your side, it’s critical to be prepared and ensure all paperwork is accurate, as they will be looking for any discrepancies they can use to deny your claim. Additionally, you should also be aware of the different legal requirements for filing a disability claim, as well as any state-specific laws or regulations that may be relevant.

Finally, having a knowledgeable and experienced disability attorney can be invaluable in helping your claim to be successful.

Have you been denied your disability benefits?

At Roy Law Group, we have been battling disability insurance cases and nothing else since 2009. This area of law is incredibly complicated, and insurance companies have endless resources available to battle your case. Let our team of experts help you. If we take on your case, you are in a winning battle.

Contact us to learn how we can help you today.

Source for disability statistics: Council for Disability Awareness

This post was originally published on November 16, 2017 but has since been updated for accuracy and relevancy.